E-Invoicing (Fatoorah) is the mandatory process of issuing, exchanging, and storing tax invoices and related notes in a structured digital format through an integrated electronic system. In Saudi Arabia, the Zakat, Tax and Customs Authority (ZATCA) requires VAT-registered businesses to generate invoices, credit notes, and debit notes electronically to ensure standardized, secure, and transparent transaction records. This system helps ensure that transactions, including domestic sales and exports, follow a consistent digital format and cannot be altered once issued.

Phase 1 - Generation Phase

Effective December 4, 2021, all VAT-registered businesses must generate and store tax invoices and electronic notes through a ZATCA-compliant e-invoicing system.

Invoices must be issued using electronic systems such as cloud platforms, POS systems, or installed invoicing software. Manual handwritten invoices are not permitted.

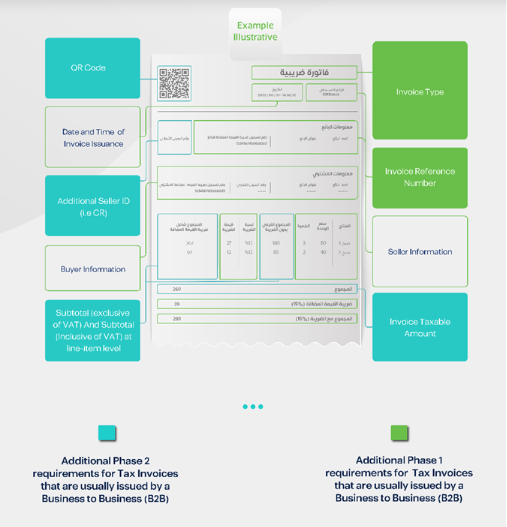

Mandatory invoice fields must be included such as VAT number, timestamp, VAT amount, and total transaction value.

Simplified invoices for B2C transactions must include a QR code to allow quick verification by customers.

Invoices are generated and stored electronically but do not need to be reported to ZATCA during this phase.

Phase 2 - Integration Phase

Effective January 1, 2023, businesses must integrate their invoicing systems with the ZATCA Fatoora platform to enable invoice validation and reporting.

E-invoices must follow approved formats such as XML or PDF/A-3 with embedded XML to ensure compliance and validation.

Systems must support secure API integration with ZATCA to allow invoice clearance and reporting.

Each invoice must include UUID, digital signatures, cryptographic stamps, and invoice hashing for security.

ZATCA implements this phase in waves and businesses are notified at least six months before integration.